Insights

January 2026

Q4 25 insights – Global Equity Strategy

Note on Performance Information

In accordance with Article (4) of Commission Regulation (EU) No 583/2010, implementing Directive 2009/65/EC (the UCITS Directive),

Fund performance data may only be shown after 12 months of performance history

Dear Investors,

Welcome to the Aecus Global Equity Fund’s first annual commentary, summarising the period since the Fund launched on 23 June 2025 to 31 December 2025.

In this report, we outline our thoughts on the portfolio fundamentals, the share price performance of our companies, specific topics that have preoccupied us as an investment team, portfolio moves we have made over the period and our outlook for the road ahead. Please note that, in accordance with European regulation, we are unable to provide fund performance statistics, until the Fund has a complete 12-months performance history.

Portfolio Fundamentals

Portfolio companies delivered strong growth since inception, with organic sales growth (our preferred growth metric) averaging +9.9% during Q2 and Q3 2025. In addition, the average portfolio company’s earnings forecast rose +8.0% since the Fund launch, consistent with expectations of low-double-digit annual earnings compounding. Most of our businesses performed well, with the primary area of market weakness being US housing (where we have little).

A few highlights:

-

- Amazon’s cloud business returned to 20% year-over-year growth, its fastest rate in three years, with strong margins from both AI and non-AI workloads.

- Idexx Laboratories, the leading veterinary diagnostics provider, delivered +12.2% organic growth last quarter, the fastest pace in four years, despite clinic traffic yet to inflect.

- Mastercard’s organic growth averaged +14.5% in the period, with robust trends across both the affluent and mass-market consumers. Notably, the company facilitated its first “Agent Pay” transaction in September, with global rollout expected in early 2026.

Some disappointments:

-

- Texas Instruments is guiding for around 10% earnings growth year on year which fell short of market expectations due a normalisation of the pace of recovery in H2.

- WillScot, the largest mobile office and storage rental provider in the US, exited a tough year with underlying revenue down 1.3% year-over-year. The new management team is focusing on improving asset efficiency to drive better revenue and profit growth in 2026.

Portfolio Performance Update

Following the first 12 months of the Fund, we will be providing Fund performance data and performance attribution information regarding key contributors and detractors.

The Fund launched with an opening NAV of 100.0000[1] on 23 June 2025, which increased to 103.7973[2] by 31 December 2025. Whilst this is a solid result for a 6-month period in absolute terms, the Fund performance was negatively impacted by some declines in valuation multiples. The NTM P/E[3] of the Fund fell from 26.0x at inception to 25.1x at the end of Q4, while the Fund’s earnings per share increased 6%.

During the same period, the reference index of the Fund, MSCI ACWI Net TR gained +14.7%. Our Fund did not keep pace with the broader market, the main reason being our lack of “US big tech”, which accounted for 70% of the underperformance vs the index. The majority of the remaining underperformance stemmed from three specific stock holdings: Pool Corp (-22%), WillScot (-29%), and Verisk Analytics (-27%).

Top contributors were broadly based:

-

- Western Digital’s strong earnings growth was driven by robust storage demand and tight hard disk supply, making it one of the top-performing shares of 2025.

- Illumina, the global leader in gene sequencing tools, has turned the page. Under a new management team, the company refocused on its core business and is set to deliver high-single-digit revenue growth and double-digits EPS growth in coming years.

- Donaldson, an industrial filter maker, continued to gain market share during the recent end-market downturn. With both China and Europe returning to growth, we anticipate Donaldson will compound annual revenue at mid-single-digit and earnings at double-digits going forward.

The detractors can be summarised in three groups:

-

- US housing activities continued to dwindle reaching new cyclical lows in 2025. This led to sharp deratings at Pool Corp and Home Depot, despite both being differentiated quality franchises.

- Companies in late stages of business turnaround, such as CoStar, Texas Instruments, and WillScot faced continued pressure in 2025, driving poor earnings momentum. We think self-help at these companies will drive better margin and cash flow in 2026.

- Software holdings such as Bentley Systems and Verisk Analytics went out of favour due to AI disruption fears. We think both businesses are deeply entrenched in their verticals making them the AI enabler for their customers.

What have we been thinking about?

Delivering consistent returns through the cycle is, in our view, best achieved by identifying defendable, repeatable, and scalable (DRS) businesses at reasonable valuations. Consequently, we diligently examine our portfolio to weed out non-compliant companies and consider opportunities that complement our existing holdings.

-

- We have increased our confidence in Tencent‘s earnings sustainability, driven by their strategic focus on investing in AI talent, rather than depreciating hardware. This positions the company favourably for long-term success in China’s AI market. Our conviction in MSCI and Verisk‘s earnings resilience has also strengthened, underpinned by their established positions as industry benchmarks.

- Several companies are well-positioned for near-term earnings growth, with tangible drivers emerging. Amazon‘s strategic investment in infrastructure, including chips and power, positions it to capitalise on growing demand from AI partners like Anthropic. Waters is transitioning its Empower software, the industry standard for chemical analysis, to a SaaS model. Meanwhile, Western Digital has brought forward its tech roadmap to address robust customer demand.

- Additionally, certain companies are pursuing scalable growth opportunities beyond their existing addressable markets. Cadence Design Systems is leveraging Intel’s management transition to expand its market share, while Mastercard is rapidly integrating Agent Pay and stablecoin capabilities into its network, broadening its offerings.

Macro from micro

The macroeconomic environment remained mixed, with divergent views on economic prospects. In the industrial space, we observed early signs of improvement.

-

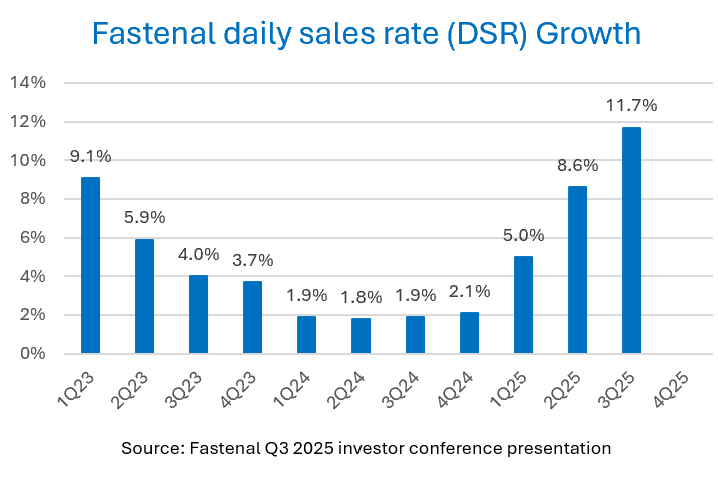

- Fastenal reported robust daily sales growth, indicating strengthening demand from manufacturing and construction end markets.

-

- Japan’s machine tool orders turned positive for the first time since 2022, hinting at a resurgence in precision manufacturing investment.

However, consumer sentiment remained subdued, with the US government shutdown and AI-driven automation concerns contributing to elevated levels of job cuts. Home Depot notes a sluggish recovery in consumer spending, despite a substantial $50 billion underspend in home repair and remodelling over the past two years.

Artificial Intelligence

The theme of AI dominated capital markets in 2025, with performance highly concentrated in a few names closely tied to AI infrastructure buildout. The big question is whether the AI scaling law will continue, to justify ongoing capex spending. We don’t have an answer to this question, but given most tech companies have front-loaded capex investments, we believe the AI rally should broaden in 2026, particularly to include companies who could benefit from adopting the technology.

34% of our portfolio comprises companies implementing AI to enhance their competitive positioning and drive earnings growth. Despite receiving little market attention so far, our enthusiasm remains unabated. Let’s look at a few examples:

-

- Mastercard‘s pilot with OpenAI on Agent Pay breaks large transactions into smaller ones, boosting financial performance and generating more granular, valuable data assets to widen its moat.

- MSCI sees AI creating new distribution channels and data consumption models, leveraging its formidable, hard-to-replicate database covering $50 trillion of financial assets.

Beyond these obvious AI beneficiaries, we’re also seeing opportunities in companies previously considered ‘non-AI’, where AI is now driving growth.

-

- Hoya, Japan’s leading lens maker, is seeing AI-driven demand across multiple fronts: optics for datacenter networking, hard disk substrates for storage demand, and camera lenses for AI-enabled smart glasses.

We remain confident that as the AI wave matures, our portfolio companies will emerge stronger, providing a solid foundation for long-term capital growth.

Portfolio moves

Since inception to the end of 2025, we built four new positions:

-

- Western Digital, a Hard Disk Drive (HDD) maker. Over 90% of the company’s revenue comes from data centre customers, who are struggling to meet the rising data storage demand in the age of AI.

- Nippon Paint, the leading paint maker in Asia. We are attracted by its leading market share in key growth markets such as China, Southeast Asia, and Turkey.

- We bought a position in Arista Network, a leading datacenter networking solution provider. Networking requirements are growing, creating multi-year growth opportunities for Arista.

- We also dipped into Disco, a Japanese semi-cap with 75% global market share in wafer dicers. Rising chip complexity and larger die size are making dicers a more critical and valuable part of the supply chain.

During H2 we exited our position in Qualcomm after a strong rally triggered by the craze for AI.

Outlook

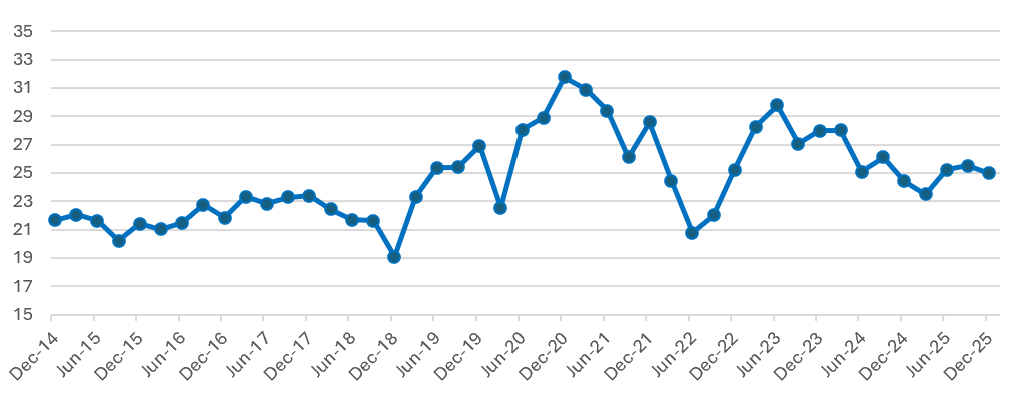

At the end of 2025, the average P/E multiple for the Fund was 25.0x, slightly above the 10-year average for these stocks of 24.6x4. Based on consensus estimates, the portfolio offers an attractive +14.5% compounded earnings growth for the next three years. We are confident that this portfolio can deliver low double digit returns consistently over the long term.

Portfolio simulation: Next 12 months Price / Earnings[4]

When the market leadership is concentrated in so few big US tech names, a balanced portfolio such as this Fund will understandably lag short term market returns. However, the +9.9% organic sales growth and +8.0% earnings upgrades to our portfolio companies over the past six months illustrate the long-term growth potential of this portfolio. Muted market sentiment on the durable franchises we favour have created attractive opportunities for active managers like us. We will continue to fine tune the portfolio, recycling capital into the most promising long-term compounders while remaining disciplined on valuation.

We warmly welcome your questions and comments.

Until next quarter,

Fan, Arnaud and Alistair

[1] NAV of the Aecus Global Equity Fund A EUR Acc Share Class.

[2] NAV of the Aecus Global Equity Fund A EUR Acc Share Class. For regulatory reasons we are unable to disclose portfolio returns until 12 months have lapsed.

[3] Next twelve months Price / Earnings ratio

[4] Source: LSEG Workspace/Aecus Partners as of 31/12/2025. Aecus Global Equity Fund Price/Earnings based on LSEG Workspace market consensus. Portfolio as of 31 December 2025, rebalanced quarterly back in time. Where a position was not yet listed, the portfolio was rebalanced excluding that stock.

Important Information

Issued by Aecus Partners SAS which is regulated by the Autorité des Marchés Financiers (AMF). RCS Paris n° 933 708 976 Agrément AMF n°GP20240027 (https://www.amf-france.org/fr, 17 place de la Bourse – 75002 Paris). The Fund is a sub-fund of the ICAV, an umbrella fund with segregated liability between sub-funds. The Fund is authorised by the Central Bank of Ireland as a UCITS pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations. The ICAV has delegated UCITS management company functions to Aecus Partners SAS as its UCITS management company. The ICAV is authorised by the Central Bank of Ireland pursuant to the Regulations and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in Transferable Securities) Regulations. The distributor of the Fund is Aecus Partners SAS. This financial promotion has been approved by Zeyro (FRN 1001386) on 15 January 2026. This Fund may be suitable for investors seeking long-term capital growth from European equities, who can commit to a five-year investment horizon and tolerate medium volatility and potential capital loss. It is not suitable for investors requiring capital protection, guaranteed returns, or access to capital within five years.

This document is a communication for information purposes only intended for professional clients. Please refer to the Fund’s prospectus and key information document before making any final investment decision. These documents are available free of charge, in paper or electronic format, from the Fund’s Investment Manager, as well as on the Manager’s website: https://www.aecuspartners.com.

This material may not be copied, reproduced, communicated or redistributed, in whole or in part, without prior authorisation from Aecus Partners SAS. Any entity responsible for forwarding this material to other parties takes responsibility for ensuring compliance with applicable financial promotion rules. This material does not constitute a subscription offer and cannot be equated with a recommendation or investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. Any specific securities identified and/or described in this document do not represent all the securities purchased, sold, or recommended for the Fund and no assumptions should be made that the securities identified and discussed were or will be profitable. The information contained in this material may be partial information and may be modified without prior notice. It is not individually tailored for or directed to any particular client or prospective client. Prospective investors should consult their financial adviser before making an investment decision.

The sources used to carry out this reporting are considered reliable, however no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Aecus Partners SAS, its officers, employees or agents. Aecus Partners SAS accepts no responsibility for any direct or indirect losses caused by the use of the information provided in this document.

All data is as at the document date unless indicated otherwise. Performance data herein relates to the Aecus Global Equity Fund (the “Fund”). Net asset value performance (NAV) data has been calculated on a NAV-to-NAV basis and is net of management fees and operating expenses, with any income reinvested. A detailed description of the charges that apply is set out in the Prospectus. The ongoing charges figure may change over time. Company holdings and performance are likely to have changed since the report date. Company information, including performance calculations and other data, is provided by Aecus Partners SAS. Past performance may not be a reliable guide to future performance and investors may not get back the amount invested. If an investor’s own currency is different from the currency in which the Fund is denominated, the investment return may increase or decrease as a result of currency fluctuations. All investments involve risk. The value of the investment and the income from it will vary. The figures quoted relate to past periods and past performance is not a reliable indicator of future performance. The Fund uses the MSCI ACWI Net Index (source: MSCI) as a comparator benchmark to compare performance. The Fund is actively managed and is not constrained by any benchmark. Glossary of terms: please refer to the website. Access to funds of an ICAV managed by Aecus Partners SAS may be subject to restrictions regarding certain persons or countries.

EEA – Access to the Fund may be subject to restrictions regarding certain persons or countries. The Fund’s Prospectus and KIDs can be obtained by visiting www.aecuspartners.com/documents and are available in one of the official languages of each of the EU Member States into which the Fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). The Fund is currently notified for marketing into a number of EU Member States under the UCITS Directive.

UK – This Fund is not authorised by the UK Financial Conduct Authority (FCA). Only those share classes that have been recognised under the OFR may be marketed to investors in the UK. As an overseas fund recognised under the OFR, the Fund is not subject to UK sustainable investment labelling and disclosure requirements. The protections provided by the UK regulatory system, including access to the Financial Services Compensation Scheme (FSCS) and the Financial Ombudsman Service (FOS), do not apply. This document is for information purposes only and does not constitute an offer or solicitation to anyone in any jurisdiction in which such offer or solicitation is not authorised. Cancellation rights do not apply, and U.K. regulatory complaints and compensation arrangements may not apply.

Glossary of terms: please refer to the website.

Related insights

Insights

This section brings together Aecus Partners’ insights, perspectives and communications. It features a curated selection of content — podcasts, interviews, market updates and commentary — designed to share our views on portfolio companies and investment dynamics. These materials reflect our convictions at a given point in time, with the aim of providing a clear, structured and accessible perspective on complex topics.