Insights

April 2026

Q1 26 insights – Podcast Global Equity Strategy

Note on Performance Information

In accordance with Article (4) of Commission Regulation (EU) No 583/2010, implementing Directive 2009/65/EC (the UCITS Directive),

Fund performance data may only be shown after 12 months of performance history

Dear Investors,

Welcome to the Aecus Global Equity Fund’s first quarter commentary of 2026, covering the period between 31 December 2025 and 31 March 2026.

As usual, in this report, we outline our view of the portfolio fundamentals, the share price performance of our companies, the topics that have preoccupied the investment team and our outlook. Please note that as we are still within the first 12 months of the Fund, we are unable to provide performance statistics, in accordance with European regulation.

The period was marked by the war in Iran, driving significant volatility in the market. From a fundamental standpoint, while the direct exposure to the region is limited, higher oil price may feed into higher inflation and interest rates, impacting short-term earnings growth and valuation multiples. We continue to believe it is quality businesses that are best placed to face these challenges.

Valuations, meantime, have contracted further, pointing to attractive double-digit return potential for the portfolio. The full year earnings season confirmed that 2025 ended strongly for portfolio companies and leads us to look towards 2026 with confidence.

Portfolio Fundamentals

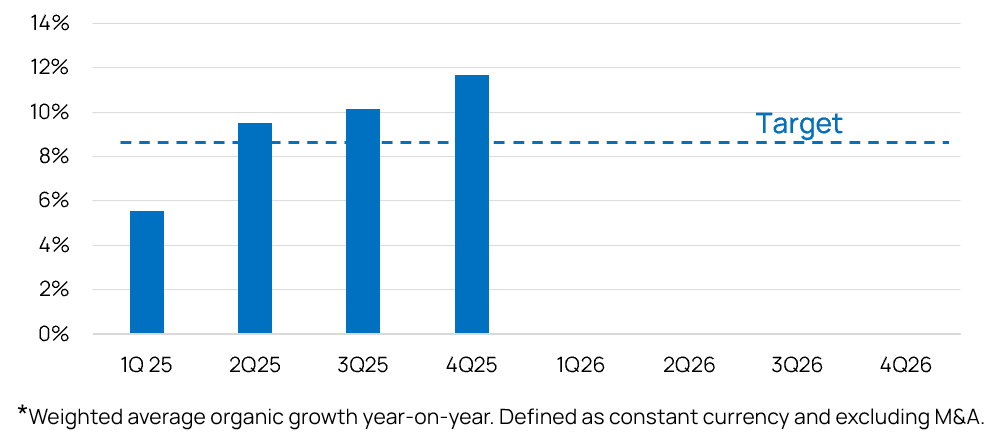

Over the past quarter, companies reported their 2025 full year results. Overall, the fundamental picture was pleasing. The average organic sales growth (our preferred growth metric) of portfolio companies reached 11.7%, ahead of the long-term historical average of 9.8%[1] for the same portfolio and ahead of our expectations.

Aecus Global Equity Fund Organic Sales Growth*

The weighted average portfolio earnings forecast rose 6.5% since the end of Q4 2025, well ahead of our expectations of low-double-digit annual earnings compounding.

A few highlights:

-

- Amazon’s cloud computing business, AWS, hit a record quarter with 24% revenue growth and 36% operating margin. Momentum is strong, with backlog up 40% year-on-year and book-to-bill ratio exceeding 2x. Capacity has doubled since 2022 and is projected to double again by 2027.

- Western Digital continues to capitalise on the data centre investment boom, posting a 25% revenue increase and a 72% surge in operating profit year-on-year. Growth visibility is improving, with shipments projected to grow over 35% in Q1 2026.

- Hoya, the Japanese optical lens leader, achieved 8% organic growth in Q4 2025. This was driven by a stabilisation in China, market share gains in Europe, and double-digit IT component sales to the semiconductors, data storage, wearables, and optical communication markets.

Some disappointments:

-

- Pool Corp, the leading U.S. pool equipment distributor, issued flat 2026 revenue guidance. Despite strategic investments in technology and footprint expansion to widen its competitive lead, high interest rates continue to weigh on demand on the low end.

- While Nintendo’s Switch 2 saw record-breaking holiday sales, high-margin software sales lagged due to a weak launch title lineup. We anticipate a turnaround in 2026, bolstered by a strong release schedule featuring blockbuster IPs such as Pokémon, Legend of Zelda, and Fire Emblem.

Portfolio Performance Update

Following the first 12 months of the Fund, we will be providing Fund performance data and performance attribution information regarding key contributors and detractors.

Despite a strong start to the year, the Fund’s NAV[2] declined from 103.9331 to 98.8911 during Q1, largely due to the impact of declines in valuation multiples triggered by the onset of the Iran war. The NTM P/E of the Fund fell from 25.1x at the end of 2025 to 22.5x at the end of Q1 2026, while earnings per share increased by 5.5%.

During the same period, the MSCI ACWI index also declined, although less than the Fund (-3.2%). Lack of exposure to the energy sector explained most of the fund’s relative underperformance. Rising 10-year US Treasury yields, triggered by the outbreak of the Iran war, had a disproportionate negative impact on long duration defensives in the portfolio, such as healthcare holdings, overshadowing an otherwise solid quarter.

Among the top contributors:

-

- Western Digital, Hoya, and KLA posted strong gains as datacentre capex continued to accelerate.

- Deere and Texas Instruments reported stronger-than-expected results, confirming that the industrial cycle has bottomed out.

Among the top detractors:

-

- Fair Isaac was caught in the crosshairs of a DOJ investigation. We expect its FICO score to remain deeply entrenched in the financial system protected by network effects and high switching costs.

- CoStar shares slumped further as investors grew weary of the margin squeeze caused by its multi-year investment in the Homes.com portal.

- Tencent’s share price softened as investors weighed ByteDance’s AI expansion against the company’s defensive strengths. We believe Tencent’s user base and integrated ecosystem will provide a robust cushion against long-term disruption.

- Healthcare stocks like Waters and IDEXX Laboratories lagged even during the market sell-off, as investors continue to rotate into high momentum technology names.

What have we been thinking about?

Faced with an extreme pace of technological change and heightened geopolitical uncertainty, we incorporate these impacts into our research, whilst remaining focused on delivering consistent returns through economic and business cycles. Our primary objective is to identify Defensible, Repeatable, and Scalable (DRS) businesses at attractive valuations. While we made several disciplined portfolio adjustments this past quarter, our confidence in the long-term growth prospects of our holdings remains unchanged.

MSCI, our top position, recently launched IndexAI Insights, allowing clients to query proprietary data using natural language. With over 120 internal AI projects underway, management expects AI to accelerate product development, including custom index, drive faster revenue growth, and enhance operating leverage.

Vulcan Materials, the largest U.S. aggregates producer, is widening its technological lead by using “Process Intelligence”, 3D sensing and AI for real-time production and precision blasting. These tech investments have boosted throughput and cut overtime, positioning the company to double EBITDA from just 15% volume growth, with any further volume recovery driving even more EBITDA upside.

Waters, our top healthcare holding, shows strong execution with new product sales up 30% to triple digits year-on-year and orders outpacing revenue. The Becton Dickinson Bioscience integration is ahead of schedule with higher synergy targets just one month after deal closing. We see over 200bps of revenue upside to conservative 2026 guidance, driven by pricing, consumables momentum, and potential recoveries in China and academic markets.

We intentionally target unique and resilient business models. We remain confident that our portfolio companies will continue to grow their earnings through fundamental long-term drivers, in spite of near-term geopolitical events.

Macro from Micro

We observe growing evidence of a cyclical recovery gaining momentum, evidenced by broad-based expansion across the trucking, industrial, and construction sectors. While this fundamental outlook is positive, near-term data may start to weaken due to the war in the Middle East. We think the potential impact will be largely binary, contingent upon the duration of the conflict and the integrity of key regional infrastructure. We continue to monitor developments closely and remain prepared to adjust our view on this nascent recovery as the situation evolves.

Below are some key observations from companies in our coverage universe.

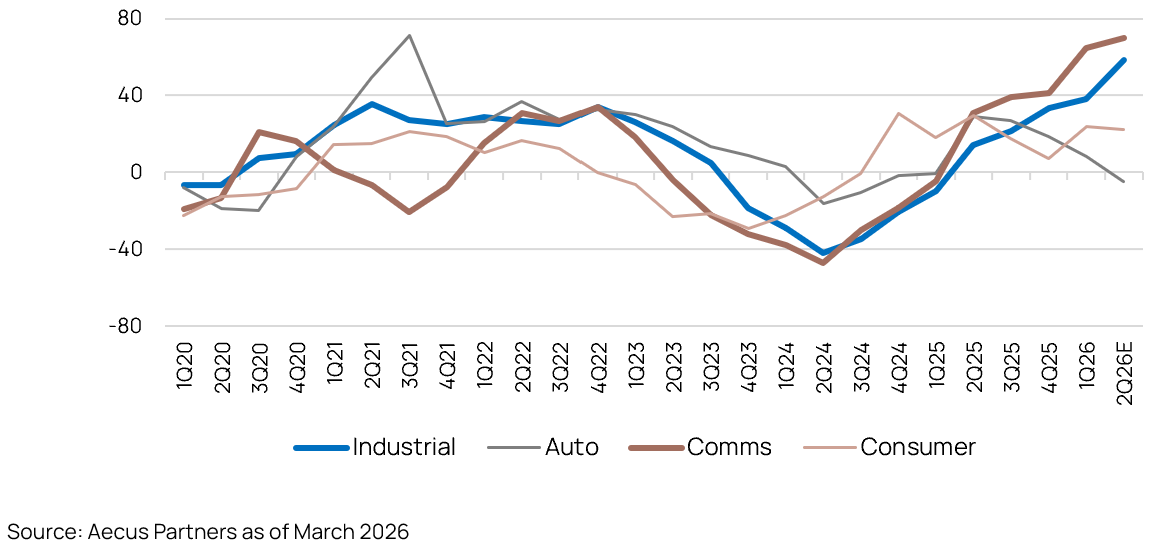

We observe a significant strengthening in the global industrial and semiconductor cycles. Analog Devices, a bellwether for the sector, reported that sales across its Industrial and Communications segments climbed between 40% and 60% year-on-year. This robust performance came despite strengthening year-ago comparisons and has led management to forecast further acceleration in the coming quarter, supported by a broad-based recovery in end-market demand.

Bellwether signs of global industrial cycle strengthening

Analog Device’s Growth Rates by End-Markets

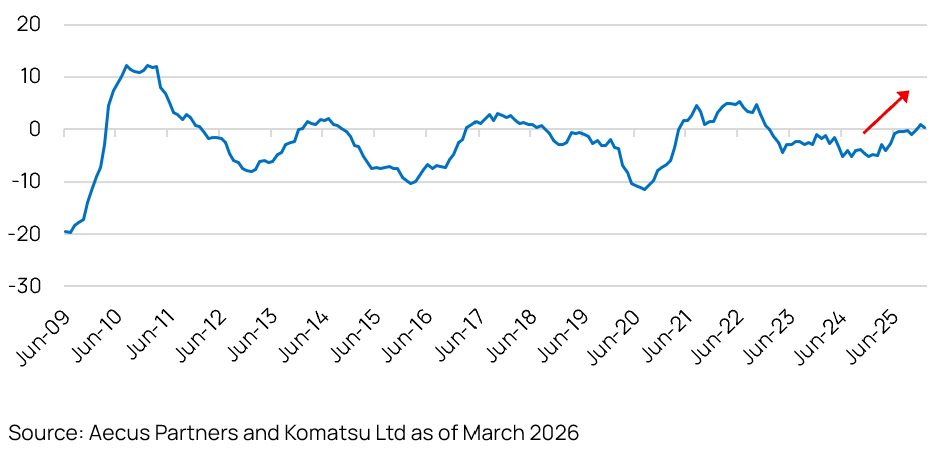

This recovery is echoed in the U.S. construction sector. Komatsu’s real-time monitoring system, Komtrax, indicates that activity has turned positive for the first time since April 2021. This inflection point aligns with the recent rebound in the ISM Manufacturing PMI, signalling an end to the three-year industrial slump.

U.S. construction activity turned positive

US Komatrax year-on-year

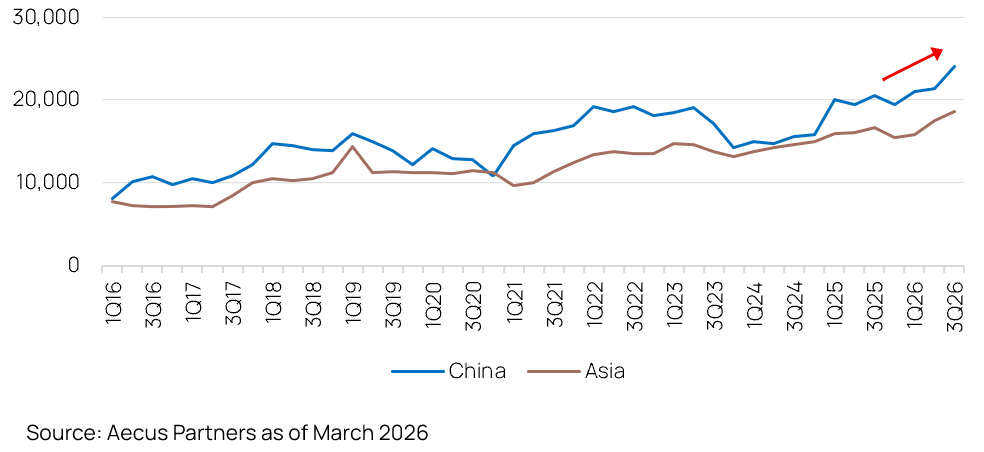

These trends extend into Asia, where distributor sales surged in late 2025. Misumi reported significant sales pickups across China and APAC. This momentum is expected to persist through 2026, driven by strong appetite for machine parts.

Surge in China and APAC industrial demand

Misumi China and Asia Sales

Artificial Intelligence

The debate over data centre (DC) capex sustainability intensified in Q1 2026, following pledges from the four major U.S. hyperscalers to increase spending by 60%, exceeding $600 billion in 2026. Including independent AI labs and Chinese internet giants, global DC capex is projected to surpass $1 trillion by 2027, roughly five times 2022 levels. Foundry giant TSMC recently raised its capex budget by 40% with further acceleration in 2027, significantly ahead of expectations.

Given the scale of this capital cycle, we maintain a disciplined, data-centric approach backed by hard evidence our investment decisions. While the revenue required to support such a buildout remains an open debate, we currently observe few signs of irrational speculation in our coverage universe.

We see AI as a transformative technology with immense real-world potential, far beyond “statistical curve fitting” or advanced autocomplete. This was proven a decade ago when an AI program, AlphaGo, defeated world “Go” champion Lee Sedol. By mastering Go, a game too complex for brute-force calculation, AI demonstrated a breakthrough in strategic reasoning and creative problem-solving. Unlike traditional models, deep learning can solve problems with incomplete information, mirroring human intelligence.

Large Language Models (LLMs) are already demonstrating transformative utility and driving progress. For example, AI’s advanced pattern recognition capabilities have turned low-radiation, non-contrast CT scans into viable tools for mass cancer screening. Beyond healthcare, LLMs are solving frontier mathematical problems and accelerating scientific research. Donald Knuth, the Turing award winner and “father of the analysis of algorithms,” was astonished by the capabilities of Anthropic’s Claude Opus 4.6, prompting a revision of his stance on generative AI.

Before AI’s full potential becomes apparent to the general public, the global adoption is occurring at an incredible pace. Gemini’s AI token[3] consumption increased over 100x between February 2024 and October 2025. Anthropic’s rapid revenue growth suggests a nearly 20x increase in token consumption since early 2025. The scale of consumption in China is even more staggering. AI adoption is also reshaping the internet traffic. Cloudflare projects that AI agent traffic will exceed human traffic by 2027, as agents typically engage 1000X more websites than human users do.

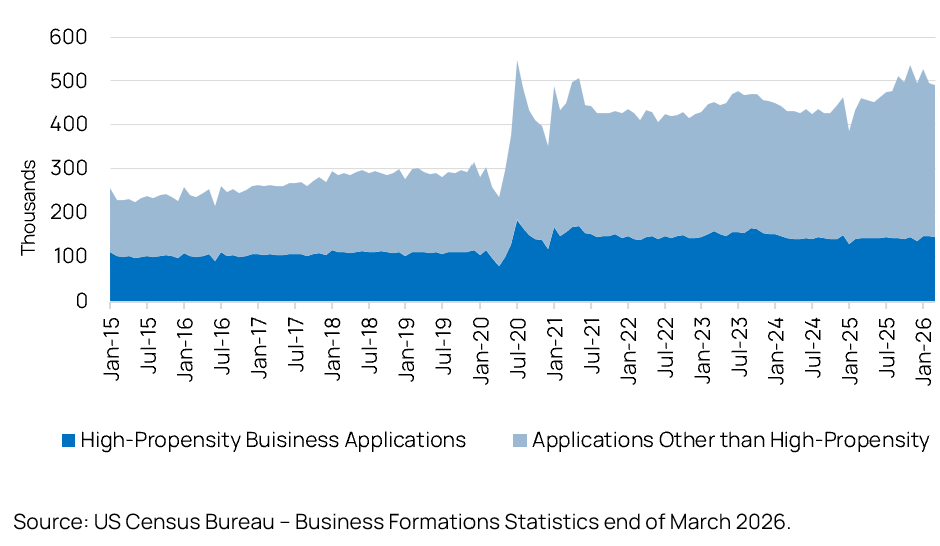

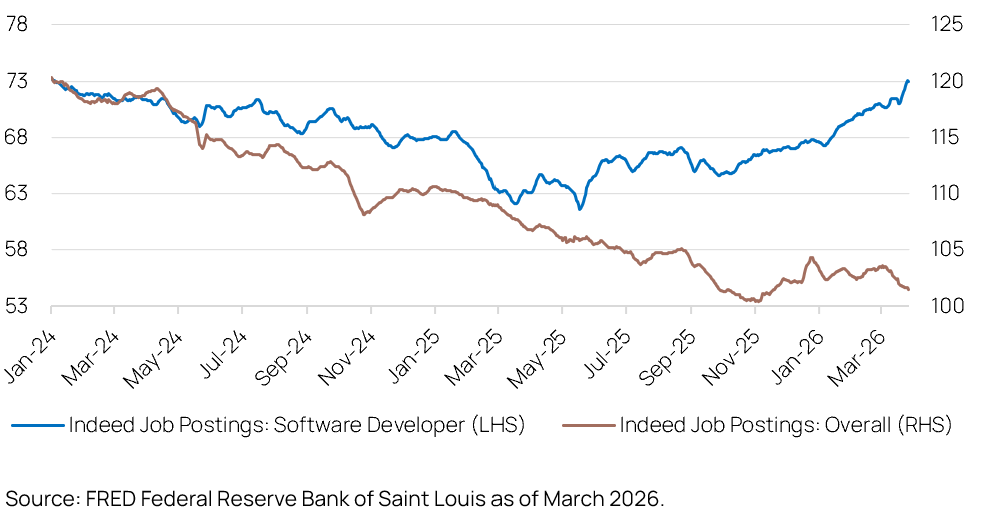

However, unconstrained adoption of AI would pose risks for our society. Anthropic acknowledged the possibility of AI automating a significant portion of human labour, potentially leading to job displacement and mass layoffs. We monitor this risk closely. So far, the “doomsday” labour scenario has yet to materialise. On the contrary, US business formation has accelerated to post pandemic highs. Indeed, the Job Postings Index for software developers is at its highest level in over two years. Furthermore, the launch of subscription-based mobile apps has surged in recent months, allaying the disruption fear.

Monthly US Business Applications

Job postings for software developers are rapidly expanding

Indeed Job Postings: Software Developer vs Overall

New subscriptions Apps launched per month (Feb 2022 – Feb 2026)

AI is deeply embedded into the operating environment and competitive dynamics of the companies we cover. We will continue to evaluate the technological momentum, commercial potential, and economical impact, to ensure the soundness and robustness of our investment thesis.

Portfolio Moves

As a result of the heightened activities and shifting technology landscape, we exited Bentley and Verisk Analytics, given lack of earnings upgrades and potential risks posed by AI. We took profit on Home Depot and recycled the capital into faster growing businesses. We started three new positions, Cognex, Murata, and Jenoptik, which are all geared to the cyclical recovery with technology angles. We also took advantage of the market weakness to top up Amazon and Nintendo, and we trimmed Texas Instruments on strength.

Outlook

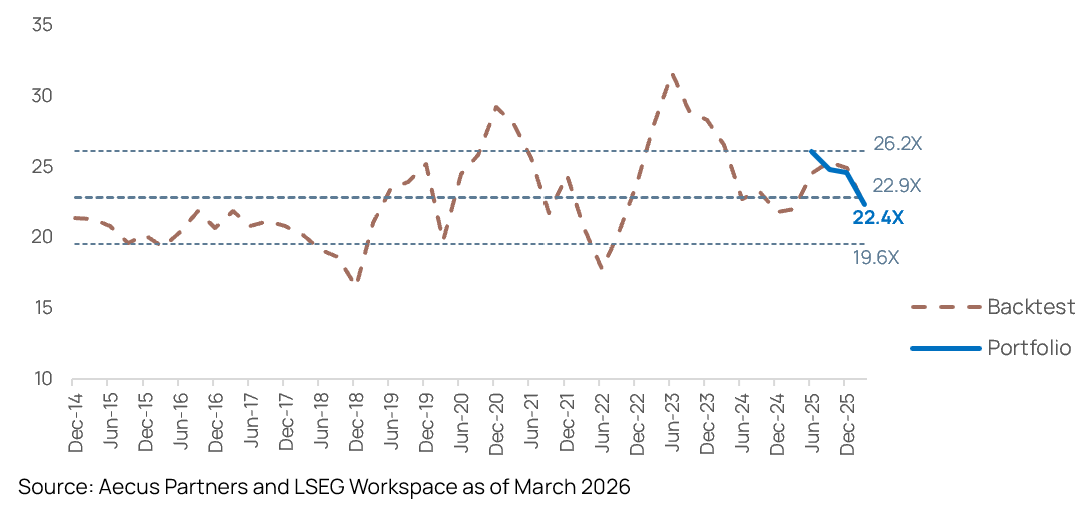

At the end of Q1, the average P/E multiple for the Fund was 22.5x, below the 10-year average for these portfolio companies of 24.6x. Based on consensus estimates and our proprietary Total Shareholder Return valuation model, we believe the portfolio offers an attractive mid double-digit compounded earnings growth for the next three years. We are confident that this portfolio can deliver double-digit returns consistently over the long term.

Simulated portfolio: valuation backtest – Current portfolio (NTM P/E)[4]

When market leadership becomes increasingly fickle, the attractiveness of truly durable franchises with growing earnings power increases. We scrutinise our portfolio companies closely and strive to maintain the balance between competitive advantage, financial outlook and valuation. We believe our approach should yield superior shareholder returns over the long run.

We thank you again for your interest in the Fund and warmly welcome you questions and comments.

Until next quarter,

Fan, Arnaud and Alistair

[1]asset weighted organic sales growth of the portfolio as of 31st of March 2026 using a 10-year average for portfolio companies of the Aecus Global Equity Fund. Source Aecus Partners

[2] S USD ACC share class of the Aecus Global Equity Fund

[3] Tokens are the fundamental units of text that AI models use to process natural language.

[4] Source: LSEG Workspace/Aecus Partners as of 26/03/2026.

Note for the Backtest: Simulated Price to Earnings for the next twelve months (NTM P/E) using the portfolio of the Aecus Global Equity Fund portfolio as of 26/03/2026. Portfolio weights as of 26 March 2026, rebalanced quarterly back in time. For any date of the simulation when a position was not yet listed, the portfolio was rebalanced excluding that stock. This does not reflect the actual portfolio P/E since launch, but a simulated calculation of a static portfolio measure for illustration purpose.

The actual NTM P/E (ex-Cash) of the Aecus Global Equity Fund since launch in June 2025 is shown separately in the blue line.

Important Information

Issued by Aecus Partners SAS which is regulated by the Autorité des Marchés Financiers (AMF). RCS Paris n° 933 708 976 Agrément AMF n°GP20240027 (https://www.amf-france.org/fr, 17 place de la Bourse – 75002 Paris). The Fund is a sub-fund of the ICAV, an umbrella fund with segregated liability between sub-funds. The Fund is authorised by the Central Bank of Ireland as a UCITS pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations. The ICAV has delegated UCITS management company functions to Aecus Partners SAS as its UCITS management company. The ICAV is authorised by the Central Bank of Ireland pursuant to the Regulations and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in Transferable Securities) Regulations. The distributor of the Fund is Aecus Partners SAS. This financial promotion has been approved by Zeyro (FRN 1001386) on 15 April 2026. This Fund may be suitable for investors seeking long-term capital growth from Global equities, who can commit to a five-year investment horizon and tolerate medium volatility and potential capital loss. It is not suitable for investors requiring capital protection, guaranteed returns, or access to capital within five years.

This document is a communication for information purposes only intended for professional clients. Please refer to the Fund’s prospectus and key information document before making any final investment decision. These documents are available free of charge, in paper or electronic format, from the Fund’s Investment Manager, as well as on the Manager’s website: https://www.aecuspartners.com. This material may not be copied, reproduced, communicated or redistributed, in whole or in part, without prior authorisation from Aecus Partners SAS. Any entity responsible for forwarding this material to other parties takes responsibility for ensuring compliance with applicable financial promotion rules. This material does not constitute a subscription offer and cannot be equated with a recommendation or investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. Any specific securities identified and/or described in this document do not represent all of the securities purchased, sold, or recommended for the Fund and no assumptions should be made that the securities identified and discussed were or will be profitable. The information contained in this material may be partial information and may be modified without prior notice. It is not individually tailored for or directed to any particular client or prospective client. Prospective investors should consult their financial adviser before making an investment decision. The sources used to carry out this reporting are considered reliable, however no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Aecus Partners SAS, its officers, employees or agents. Aecus Partners SAS accepts no responsibility for any direct or indirect losses caused by the use of the information provided in this document.

All data is as at the document date unless indicated otherwise. Performance data herein relates to the Aecus Global Equity Fund (the “Fund”). Net asset value performance (NAV) data has been calculated on a NAV-to-NAV basis and is net of management fees and operating expenses, with any income reinvested. A detailed description of the charges that apply is set out in the Prospectus. The ongoing charges figure may change over time. Company holdings and performance are likely to have changed since the report date. Company information, including performance calculations and other data, is provided by Aecus Partners SAS. Past performance may not be a reliable guide to future performance and investors may not get back the amount invested. If an investor’s own currency is different from the currency in which the Fund is denominated, the investment return may increase or decrease as a result of currency fluctuations. All investments involve risk. The value of the investment and the income from it will vary. The figures quoted relate to past periods and past performance is not a reliable indicator of future performance. The Fund uses the MSCI ACWI Net Index (source: MSCI) as a comparator benchmark to compare performance. The Fund is actively managed and is not constrained by any benchmark. Glossary of terms: please refer to the website. Access to funds of an ICAV managed by Aecus Partners SAS may be subject to restrictions regarding certain persons or countries.

EEA – Access to the Fund may be subject to restrictions regarding certain persons or countries. The Fund’s Prospectus and KIDs can be obtained by visiting www.aecuspartners.com/documents and are available in one of the official languages of each of the EU Member States into which the Fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). The Fund is currently notified for marketing into a number of EU Member States under the UCITS Directive.

UK – This Fund is a sub-fund of an Irish UCITS authorised by the Central Bank of Ireland and is not authorised by the UK Financial Conduct Authority (FCA). The Fund is recognised in the United Kingdom under the Overseas Funds Regime (OFR) in respect of certain share classes only. Only those share classes that have been recognised under the OFR may be marketed to investors in the UK. As an overseas fund recognised under the OFR, the Fund is not subject to UK sustainable investment labelling and disclosure requirements. The protections provided by the UK regulatory system, including access to the Financial Services Compensation Scheme (FSCS) and the Financial Ombudsman Service (FOS), do not apply. This document is for information purposes only and does not constitute an offer or solicitation to anyone in any jurisdiction in which such offer or solicitation is not authorised. Cancellation rights do not apply, and U.K. regulatory complaints and compensation arrangements may not apply. This material is issued and approved by Aecus Partners SAS which is authorised and regulated by the Autorité des Marchés Financiers (AMF).

Glossary of terms: please refer to the website

Contacts Aecus Partners: bonjour@aecuspartners.com – +33 (0)1 84 80 81 82 – 128 rue du Faubourg Saint-Honoré – 75008 Paris

Related insights

Insights

This section brings together Aecus Partners’ insights, perspectives and communications. It features a curated selection of content — podcasts, interviews, market updates and commentary — designed to share our views on portfolio companies and investment dynamics. These materials reflect our convictions at a given point in time, with the aim of providing a clear, structured and accessible perspective on complex topics.