Insights

Sébastien Thévoux-Chabuel

Portfolio Manager, European Strategies Corporate Culture Analyst

Discover his bioJanuary 2026

Q4 25 insights – European Equity Strategy

Note on Performance Information

In accordance with Article (4) of Commission Regulation (EU) No 583/2010, implementing Directive 2009/65/EC (the UCITS Directive),

Fund performance data may only be shown after 12 months of performance history

Dear Investors,

Welcome to the Aecus Europe Equity Fund’s first annual commentary, summarising the period since the Fund launched on 30 June 2025 to 31 December 2025.

In this report, we outline our view of the portfolio fundamentals, the share price performance of our companies, the topics that have preoccupied the investment team, the portfolio moves we have made over the period and our outlook for the road ahead. Please note that as we are still within the first 12 months of the Fund, we are unable to provide fund performance statistics, in accordance with European regulation.

Portfolio Fundamentals

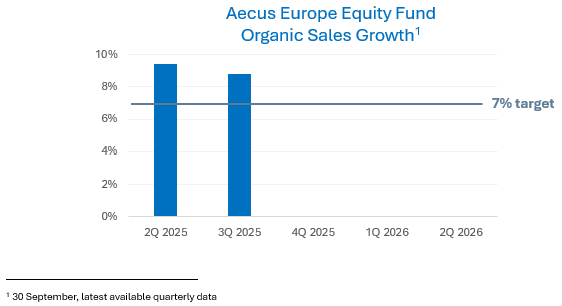

Portfolio fundamentals over H2 2025 were solid. Organic sales growth, our preferred measure, rose +9% year-over-year in the third quarter, continuing the strong dynamic witnessed in the second quarter. This is above our target level of circa 7%.

Among the companies that impressed most:

-

- Galderma, the Swiss cosmetic dermatology leader, accelerated considerably, delivering +21% organic sales growth. Strong innovation across their portfolio of biostimulators, neuromodulators and therapeutic dermatology products is driving the growth.

- Games Workshop, the UK makers of Warhammer figurine games, reported >15% core revenue growth, a remarkable feat considering this is an “off” year in their 3-year product cycle rollouts.

- Adyen, the global payments leader, delivered another solid set of results (+23% organic growth) and provided strong medium term growth guidance at their most recent capital markets day.

- Seagate Technologies, the hard disk drive manufacturer, delivered strong Q2 and Q3 results with +21% organic growth in Q3 alone, driven by continued strong datacentre demand for long term memory capacity.

There were also some disappointments:

-

- Construction names suffered over H2 2025 from the morose new build environment. Organic growth was stunted for Assa Abloy, Kingspan and Sika, however, headline total growth was overall higher, supported by M&A activity (typically our least-preferred form of growth) and efficiency measures implemented (otherwise known as cost cutting). With a combined exposure of a little over 5%, this bucket constitutes the most cyclical part of the portfolio, and we continue to monitor this closely.

- Our Beverages exposure also suffered over the period, with negative organic sales growth for Rémy Cointreau and low single digit growth for Campari. We continue to believe that most of the weakness is due to short term cyclical factors and await signs of a recovery in order for us to become more constructive with position sizing. The combined portfolio exposure has remained less than 3% over the period.

Since the Fund launched in June 2025, the weak US Dollar has generally weighed on growth, taking a full 3-points off reported Q3 growth. Around 40% of the portfolio’s revenue is derived in US Dollars or Dollar-linked currencies.

We await the full year results which will be reported in February and March 2026 but expect 2025 to have been a strong year for our portfolio companies, with overall high-single digit organic growth, double-digit earnings growth and strong free cashflow conversion.

Portfolio Performance Update

Following the first 12 months of the Fund, we will be providing Fund performance data and performance attribution information regarding key contributors and detractors.

The Fund launched with an opening NAV of 100.00002 on 30 June 2025, which fell to 94.4384[1] by 31 December. The Fund’s decline in value was predominantly driven by an overall compression in the portfolio’s valuation multiple, from 25.6x[2] at launch to 23.9x3 by year end. In contrast, over the same period the earnings per share of the Fund, our “north star”, continued to rise.

The Fund’s reference index, MSCI Europe Net TR rose +10.4%[3] over the period, driven largely by the sustained strength of the banking sector, with large constituents such as HSBC, Santander and BBVA all up over 30%. Energy companies also performed strongly, notably BP, Shell and TotalEnergies. The Fund has no exposure to these sectors as a result of our investment style.

Among the contributors:

-

- ASML performed strongly as customer investment plans to equip new AI datacenters point to growth accelerating in the coming years.

- Galderma, Games Workshop and Seagate Technologies all rose strongly on the back of stellar results, as discussed above.

Among the greatest detractors to performance:

-

- Data businesses RELX and Experian fell due to fears they may be disrupted by AI. On the contrary, we believe that such businesses owning clean, proprietary datasets will thrive in the age of AI. The intelligence tool is only as powerful as the quality of the dataset it is analysing. We added to both.

- Carl Zeiss and Rémy Cointreau both fell as earnings estimates were significantly cut. In both cases we believe they own exceptional franchises and are fundamentally undervalued but acknowledge we were too early in our positioning. Carl Zeiss is showing tentative signs that earnings are bottoming, while Rémy remains challenged by weak end markets.

What have we been thinking about?

Artificial Intelligence (AI)

Over the past two years the remarkable ramp up of hyperscaler capex has driven both equity markets and the US economy. Attention is now turning to the applications of this remarkable technology, in an attempt to establish who the winners and losers will be. Share price moves suggest the market prefers to shoot first and ask questions later, as evidenced by indiscriminatory declines in most software and data businesses.

In our view AI will, in aggregate, be more of an opportunity than a threat. There will no doubt be a lot of disruption, but for most it will be a remarkable productivity tool and, provided there is pricing power, companies should be able to hold onto those savings. Around 65% of the portfolio companies sell “things” (e.g. Lindt, L’Oréal, Games Workshop, Coloplast) where we see limited AI disruption risk and, instead, see productivity opportunities.

For the remaining 35%, we have circa 13% exposure to companies involved in the AI infrastructure buildout (ASML, VAT, Seagate Technologies and Schneider Electric) and 10% exposure to data businesses where we see AI as an opportunity (RELX and Experian). We took advantage of recent share price weaknesses to top up.

Where we see the greatest risk is in services companies, where we have little exposure and which led us to divest our holding in Accenture.

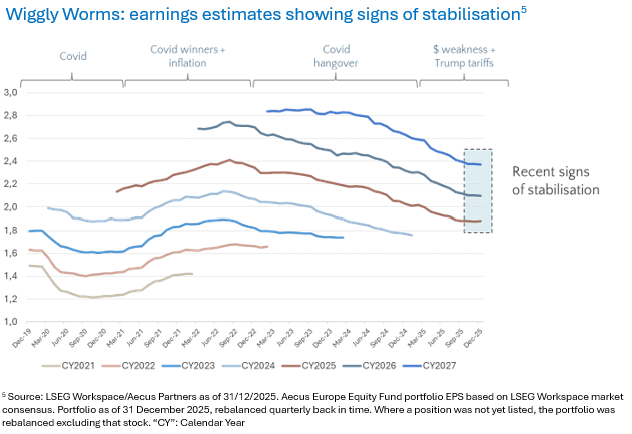

Our “Wiggly Worms” – quality companies have been on a covid-induced rollercoaster, but there are signs of stabilisation

Since Covid hit in March 2020, we have witnessed an earnings wave for many “quality” companies, the effects of which are still being felt. Below we show the aggregate of portfolio companies’ “Wiggly Worms”, a representation of how the earnings estimates have changed over time[4]. Each “worm” represents the evolution of a given year’s estimated earnings per share, ending in each case with the actual earnings outcome. It allows us to track how expectations change through time and whether businesses are surprising positively or negatively.

There are broadly four phases:

-

- In the first phase, earnings estimates fell as Covid hit.

- In the second phase those estimates not only recovered but went on to surpass the levels first forecast. Far from suffering, many well-established quality businesses came out of Covid with even stronger earnings than expected before the pandemic. Consumers, who had stayed indoors and saved in 2020 and 2021, went out to buy L’Oréal’s beauty products and socialise with friends over an Aperol Spritz. Dental practices reopened and construction projects resumed in full swing. Much of the pent-up demand induced by Covid returned at once, and the quality businesses generally benefitted the most through accelerated market share gains.

- What followed, however, was an earnings hangover as these companies’ estimates were consistently cut between mid-2022 and October 2025. In essence, quality companies had over-earned in 2021 and 2022 and the rate of market share gains, which had been forecast to continue, normalised. Earnings still grew, but at a slower rate than expected.

- This phenomenon was compounded in 2025 by the weakening of the US Dollar and Trump’s tariffs, both of which broadly hurt international businesses the most and led to another wave of downgrades.

- Over the final months of 2025 we have seen signs that earnings estimates are stabilising. While it is too early to call this a trend, we view this as encouraging. And, in our view, a necessary condition for valuations of the portfolio’s companies to stabilise.

Healthcare

The portfolio’s largest exposure is to the Healthcare sector (30%), which is currently trading on decade low valuations. With a broad range of companies and drivers of returns in this sector, our bottom-up stock selection leads us to companies such as medical device businesses rather than pharmaceutical companies, as we view the franchises to be more defendable and less at risk from price controls. Despite being out of favour, we continue to like the structural growth backdrop: US annual healthcare spending has never fallen since records began. Furthermore, we see innovation as a key driver of growth. For example, Carl Zeiss’ new laser eye surgery tool cuts an operation down from up to a minute to a few seconds, removing an important deterrent for potential new patients.

Tariffs and pricing power

From our interactions with portfolio companies, we note that many withheld from initially pushing through price increases in 2025 to offset US tariffs, waiting instead for the tariff levels to stabilise. From H2 2025, price increases started to be implemented by those with significant pricing power and we expect this to continue and to provide a pricing tailwind to growth across the portfolio in the coming year.

Portfolio Moves

Since launch, we have built two new positions in the portfolio and exited one:

-

- We added Rémy Cointreau, the owner of one of the world’s most prestigious Cognac brands.

- We built a position in Seagate Technologies, a Hard Disk Drive (HDD) producer in the consolidated and structurally growing memory market. Artificial intelligence has created a burgeoning need for low-cost memory, and we believe Seagate is well-placed to benefit.

- We divested from Accenture as we see it as most at risk from potential AI disruption.

We also made a number of valuation-driven moves, trimming on strength (L’Oréal, Halma, Assa Abloy, Galderma) and reinvesting on weakness (RELX, Straumann, Novonesis). Since inception, the fund’s turnover is tracking at an annualised rate of around 20%, which is within our expected long-term range of 20-30%.

Outlook

Stock markets have been highly polarised of late. AI has created huge share price winners (semiconductors) and losers (software). In Europe, global uncertainty, higher interest rates and protectionism have benefitted domestic businesses, and especially banks and defence companies. International businesses, outside of the semiconductor sector, are no longer as attractive, at least in the eyes of investors.

We take a different view. The organic sales growth of the handful of international companies that constitute your portfolio has rarely been so strong, and it is not just because of AI. The pace of innovation continues to impress us, whether it be Alcon’s latest generation of cataract machines, or Straumann’s iExcel product range. EssilorLuxottica, in partnership with Meta, is seeing strong take-up of its latest smart glasses while Galderma’s numerous product launches have surpassed all expectations. Demand for what these international businesses are selling is strong, and it is being driven by innovation. They see AI as an enabler to do even more, both on innovation and to streamline their operations.

Masking this strong underlying dynamic has been the weakness of the US dollar and tariffs, which resulted in earnings downgrades, in turn depressing valuation multiples. We see signs of stabilisation and, notwithstanding further currency headwinds, expect reported earnings growth to accelerate in 2026. Even assuming a further compression of valuation multiples, we see the prospect for double digit annualised returns in the coming years, driven by strong earnings growth and cash returns.

We warmly welcome your questions and comments.

Until next quarter,

Alistair, Arnaud & Sébastien

[1] NAV of the Aecus Europe Equity Fund A EUR Acc Share Class. For regulatory reasons we are unable to disclose portfolio returns until 12 months have lapsed. Past performance may not be a reliable guide to future performance. [2] Next Twelve Months Price to Earnings ratio (NTM P/E) [3] Source: MSCI in EUR as of 31/12/2025 [4] We have simulated the portfolio’s earnings backwards using 30/11/2025 weights of the Aecus Europe Equity Fund.

Important Information

Issued by Aecus Partners SAS which is regulated by the Autorité des Marchés Financiers (AMF). RCS Paris n° 933 708 976 Agrément AMF n°GP20240027 (https://www.amf-france.org/fr, 17 place de la Bourse – 75002 Paris). The Fund is a sub-fund of the ICAV, an umbrella fund with segregated liability between sub-funds. The Fund is authorised by the Central Bank of Ireland as a UCITS pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations. The ICAV has delegated UCITS management company functions to Aecus Partners SAS as its UCITS management company. The ICAV is authorised by the Central Bank of Ireland pursuant to the Regulations and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in Transferable Securities) Regulations. The distributor of the Fund is Aecus Partners SAS. This financial promotion has been approved by Zeyro (FRN 1001386) on 15 January 2026. This Fund may be suitable for investors seeking long-term capital growth from European equities, who can commit to a five-year investment horizon and tolerate medium volatility and potential capital loss. It is not suitable for investors requiring capital protection, guaranteed returns, or access to capital within five years.

This document is a communication for information purposes only intended for professional clients. Please refer to the Fund’s prospectus and key information document before making any final investment decision. These documents are available free of charge, in paper or electronic format, from the Fund’s Investment Manager, as well as on the Manager’s website: https://www.aecuspartners.com. This material may not be copied, reproduced, communicated or redistributed, in whole or in part, without prior authorisation from Aecus Partners SAS. Any entity responsible for forwarding this material to other parties takes responsibility for ensuring compliance with applicable financial promotion rules. This material does not constitute a subscription offer and cannot be equated with a recommendation or investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. Any specific securities identified and/or described in this document do not represent all of the securities purchased, sold, or recommended for the Fund and no assumptions should be made that the securities identified and discussed were or will be profitable. The information contained in this material may be partial information and may be modified without prior notice. It is not individually tailored for or directed to any particular client or prospective client. Prospective investors should consult their financial adviser before making an investment decision. The sources used to carry out this reporting are considered reliable, however no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Aecus Partners SAS, its officers, employees or agents. Aecus Partners SAS accepts no responsibility for any direct or indirect losses caused by the use of the information provided in this document.

All data is as at the document date unless indicated otherwise. Performance data herein relates to the Aecus Europe Equity Fund (the “Fund”). Net asset value performance (NAV) data has been calculated on a NAV-to-NAV basis and is net of management fees and operating expenses, with any income reinvested. A detailed description of the charges that apply is set out in the Prospectus. The ongoing charges figure may change over time. Company holdings and performance are likely to have changed since the report date. Company information, including performance calculations and other data, is provided by Aecus Partners SAS. Past performance may not be a reliable guide to future performance and investors may not get back the amount invested. If an investor’s own currency is different from the currency in which the Fund is denominated, the investment return may increase or decrease as a result of currency fluctuations. All investments involve risk. The value of the investment and the income from it will vary. The figures quoted relate to past periods and past performance is not a reliable indicator of future performance. The Fund uses the MSCI Europe Net Index (source: MSCI) as a comparator benchmark to compare performance. The Fund is actively managed and is not constrained by any benchmark. Glossary of terms: please refer to the website. Access to funds of an ICAV managed by Aecus Partners SAS may be subject to restrictions regarding certain persons or countries.

EEA – Access to the Fund may be subject to restrictions regarding certain persons or countries. The Fund’s Prospectus and KIDs can be obtained by visiting www.aecuspartners.com/documents and are available in one of the official languages of each of the EU Member States into which the Fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). The Fund is currently notified for marketing into a number of EU Member States under the UCITS Directive.

UK – This Fund is a sub-fund of an Irish UCITS authorised by the Central Bank of Ireland and is not authorised by the UK Financial Conduct Authority (FCA). The Fund is recognised in the United Kingdom under the Overseas Funds Regime (OFR) in respect of certain share classes only. Only those share classes that have been recognised under the OFR may be marketed to investors in the UK. As an overseas fund recognised under the OFR, the Fund is not subject to UK sustainable investment labelling and disclosure requirements. The protections provided by the UK regulatory system, including access to the Financial Services Compensation Scheme (FSCS) and the Financial Ombudsman Service (FOS), do not apply. This document is for information purposes only and does not constitute an offer or solicitation to anyone in any jurisdiction in which such offer or solicitation is not authorised. Cancellation rights do not apply, and U.K. regulatory complaints and compensation arrangements may not apply. This material is issued and approved by Aecus Partners SAS which is authorised and regulated by the Autorité des Marchés Financiers (AMF).

Glossary of terms: please refer to the website

Related insights

Insights

This section brings together Aecus Partners’ insights, perspectives and communications. It features a curated selection of content — podcasts, interviews, market updates and commentary — designed to share our views on portfolio companies and investment dynamics. These materials reflect our convictions at a given point in time, with the aim of providing a clear, structured and accessible perspective on complex topics.