Insights

April 2026

Q1 26 insights – Podcast European Equity Strategy

Note on Performance Information

In accordance with Article (4) of Commission Regulation (EU) No 583/2010, implementing Directive 2009/65/EC (the UCITS Directive),

Fund performance data may only be shown after 12 months of performance history

Dear Investors,

Welcome to the Aecus Europe Equity Fund’s first quarter commentary for 2026, summarising the period from 31 December 2025 to 31 March 2026.

The period was marked by the war in Iran, driving down share prices for the market and the portfolio alike. From a fundamental standpoint, while the direct effects of the war are limited (sales exposure to the Middle East is just 2%), it is the second order impacts on inflation and interest rates that are more relevant. We continue to believe it is quality businesses that are best placed to face these challenges.

Valuations, meantime, have contracted further, pointing to attractive double-digit medium-term return potential for the portfolio. The full year earnings season confirmed that 2025 ended strongly for portfolio companies and leads us to look towards 2026 with confidence.

As usual, in this report, we outline our view of the portfolio fundamentals, the share price performance of our companies, the topics that have preoccupied the investment team, the portfolio moves we have made over the period and our outlook. Please note that as we are still within the first 12 months of the Fund, we are unable to provide fund performance statistics, in accordance with European regulation.

Portfolio Fundamentals

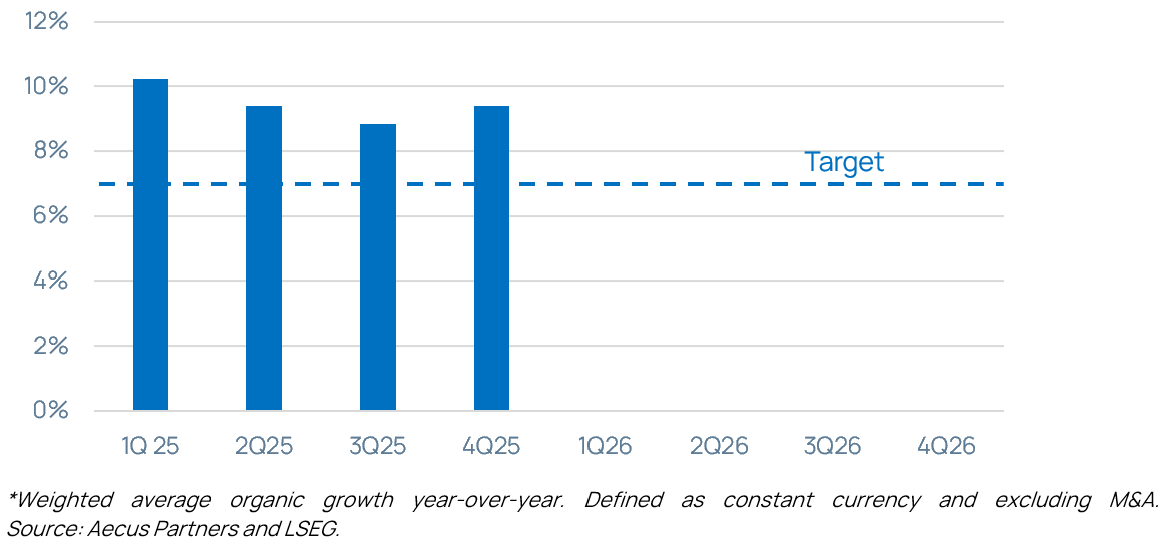

Q1 was 2025 results season

With companies reporting prior calendar year results and providing guidance for the years ahead, Q1 is always a good opportunity to take the pulse of portfolio fundamentals.

-

- Weighted average portfolio constant currency organic sales growth for 2025 was +9%, somewhat ahead of our expectations. This remains a crucial metric for us, as we believe that organic growth is the most repeatable, most visible and usually the most profitable form of growth. The weaker US Dollar led to reported sales growth of +7%, due to portfolio companies’ 35% revenue exposure to North America.

- Despite multiple macro headwinds (tariffs, currency fluctuations, geopolitical uncertainty and consumer softness), the portfolio in aggregate delivered +7% earnings per share growth. Excluding currency effects, we estimate this translates to double digit growth. The resilience of the portfolio’s earnings to tariffs and weak consumer confidence demonstrates our portfolio companies’ quality and defensive characteristics.

- 2026 guidance, for those companies who provide it, points to another strong year ahead of high-single digit organic sales growth.

Aecus Europe Equity Fund – Organic Sales Growth*

Those companies that impressed us most:

-

- Galderma, the recently listed leader in dermatological beauty, upgraded its 2025 guidance twice during the year and raised its mid-term outlook too. The company is seeing better than expected demand for its fillers and biostimulators portfolio, while also raising its peak sales estimate for Nemluvio, a patented cream for severe skin irritations. In February, L’Oréal increased its stake to 20% and has requested 2 seats on the board. We have been adding to our position.

- ASML reported a strong set of 2025 results and guided to another year of double-digit growth in 2026, despite market fears 6 months ago that revenue would decline. As we expected, the boom in datacenter and AI spending is feeding down the funnel to the only manufacturer of advanced lithography machines: ASML. It remains the portfolio’s top position.

- Campari delivered gravity-defying underlying organic growth in 4Q25 of +4.7% in a declining spirits market. The Aperol engine returned to growth while free cash flow improved handsomely.

There were also disappointments in the results season, namely:

-

- Carl Zeiss Meditec (circa 2% position) reported disappointing fiscal 2026 first quarter results and removed their FY26 guidance, just a month after it was issued. They are also searching for a new CEO. We continue to believe Carl Zeiss has amongst the best and most admired product portfolios in the industry, but we now need to gain confidence in the ability of the new management team to execute on that potential. The position remains under review.

- Dassault Systèmes (circa 2% position) issued disappointing 2026 guidance, expecting only +3-6% constant currency EPS growth. After a challenging 2025, the company has taken the decision to guide conservatively. We await evidence of stabilisation in their Life Sciences and Mainstream verticals before turning more positive.

- Lindt (circa 4% position) also issued lower than expected 2026 guidance of +4-6% organic sales growth (vs +6-8% expected). We see this as transitory, following 3 years of sharp price increases to offset cocoa cost inflation.

Portfolio Performance Update

Following the first 12 months of the Fund, we will be providing Fund performance data and performance attribution information regarding key contributors and detractors.

In Q1 the Fund’s NAV[1] fell from €94.5365 to €86.5554, whilst the MSCI Europe index fell by 0.9%.

Performance in 2026 to date has been marked by two important factors:

- AI investments continue to surprise positively, leading TSMC, the world’s leading chip manufacturer, to upgrade substantially its capital expenditure expectations. This lifted the entire semiconductor value chain, and in particular the portfolio’s holdings in Seagate Technology, ASML and VAT (and to some extent Halma).

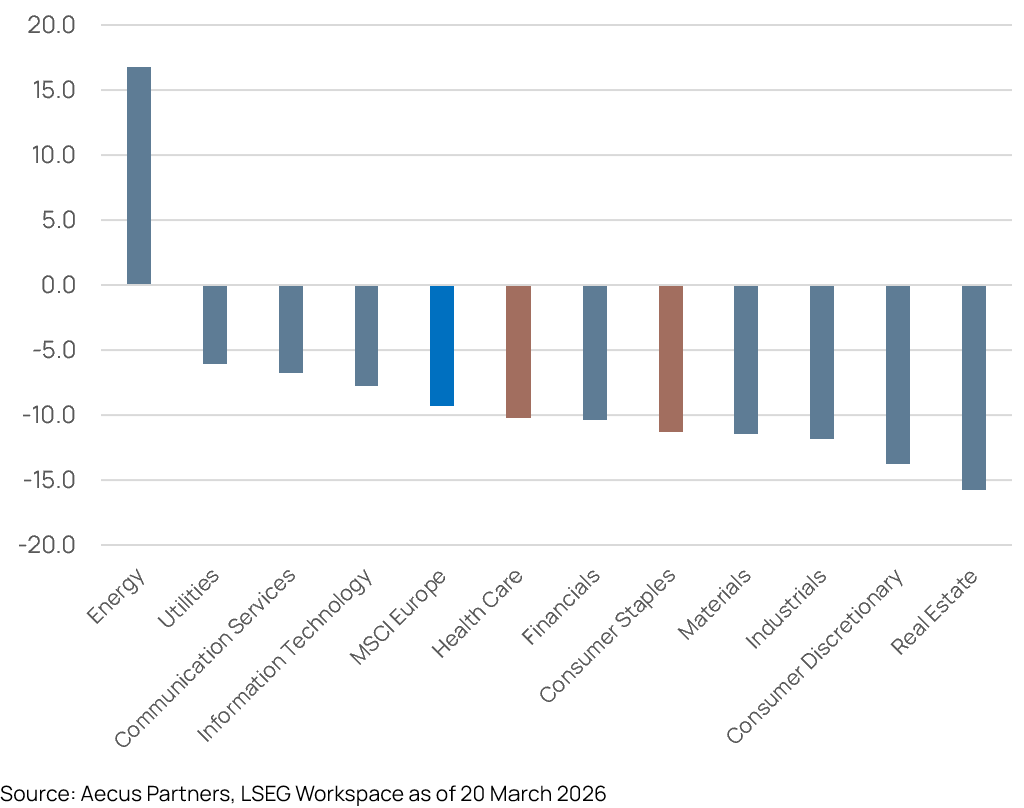

- The war in the Middle East led equity markets to fall sharply in March, with the Fund marginally underperforming in the sell-off. Traditionally defensive sectors such as Healthcare and Consumer Staples did not prove defensive, while the Energy sector rallied. This reflects the market’s continued focus on inflation and interest rates, to which the Healthcare and Consumer Staples sectors are more sensitive, rather than the economic cycle, to which these sectors are less sensitive (hence their ‘defensive’ moniker).

Sector performance (%) from start of Iran war to trough

(MSCI Europe 28/02/2026 – 20/03/2026)

The last major economic downturn was almost 20 years ago, which may explain the market’s lesser focus on cyclicality as a factor. We are of the opinion that economic cycles are not a thing of the past, and continue to prefer companies that are defensive, in the traditional sense of the term. We believe the indiscriminate nature of the selling is creating unique buying opportunities in defensive sectors.

Among the top contributors

-

- Seagate Technology, ASML and VAT all benefitted from earnings upgrades on the back of stronger than expected semiconductor spending to support datacenter buildouts.

- Campari delivered better than expected Q4 results, as discussed above.

Among the top detractors

-

- Carl Zeiss reacted to the weak results noted above.

- Coloplast continued to slide on minor earnings downgrades. The company has named a new CEO, Gavin Wood, who will start on May 1st.

- Experian, Adyen and RELX fell following Claude AI’s latest release, triggering a sell off concerning perceived “AI losers”. We added marginally to Experian and RELX on the weakness, based on the belief that not all software businesses will suffer from AI. More on this later.

What have we been thinking about?

Company research

Our main activity is researching companies, both those we own, and those we don’t. This is the most important ingredient of our long-term performance.

In addition to the usual management meetings, our investment team hit the road to meet companies at their headquarters. We travelled, among others, to Switzerland to meet VAT, to London to meet Wise and to Amersham to meet divisional management of Halma. We have further trips planned for Q2.

In addition, we worked on a number of new ideas across different sectors from LNG transportation to biscuits and from veterinary product providers to semi suppliers, mostly in the mid-cap space. We will continue to explore new ideas wherever we can to replenish our portfolio bench and create as much competition for capital as we can in the portfolio.

The impact of the War in the Middle East

The direct impacts of the war in Iran appear to be fairly limited, the Middle East accounts for just 2% of portfolio sales. The indirect implications are far more relevant, from the inflationary effects of the war, not least on consumption, to the implications for interest rates. We view these indirect impacts as part of the usual macro uncertainties companies face and believe it is quality businesses that are best armed to deal with them. Like most, we hope for a quick resolution to the conflict.

As the CFO of a portfolio company remarked to us, “running a globally active company like ours is much more challenging than it was five years ago”. Whether it be tariffs, the wars in Russia and the Middle East, supply chain stresses or currency fluctuations, global businesses do indeed face more challenges than before. Swiss companies are looking to reduce their Swiss Franc cost base due to the currency’s strength, healthcare companies are building local manufacturing presence in China to be eligible for local to local sourcing, US exposed companies are looking to optimise their supply chains to minimise the effects of tariffs, and where they can’t avoid them they are pushing through price increases. We do not believe this changes the long-term prospects for high quality global businesses – countries still want access to the best products and services and are willing to pay for it – but it sets the bar higher for innovation and operational flexibility. The ability for a company to adapt is becoming an increasingly important investment criterion in our selection process.

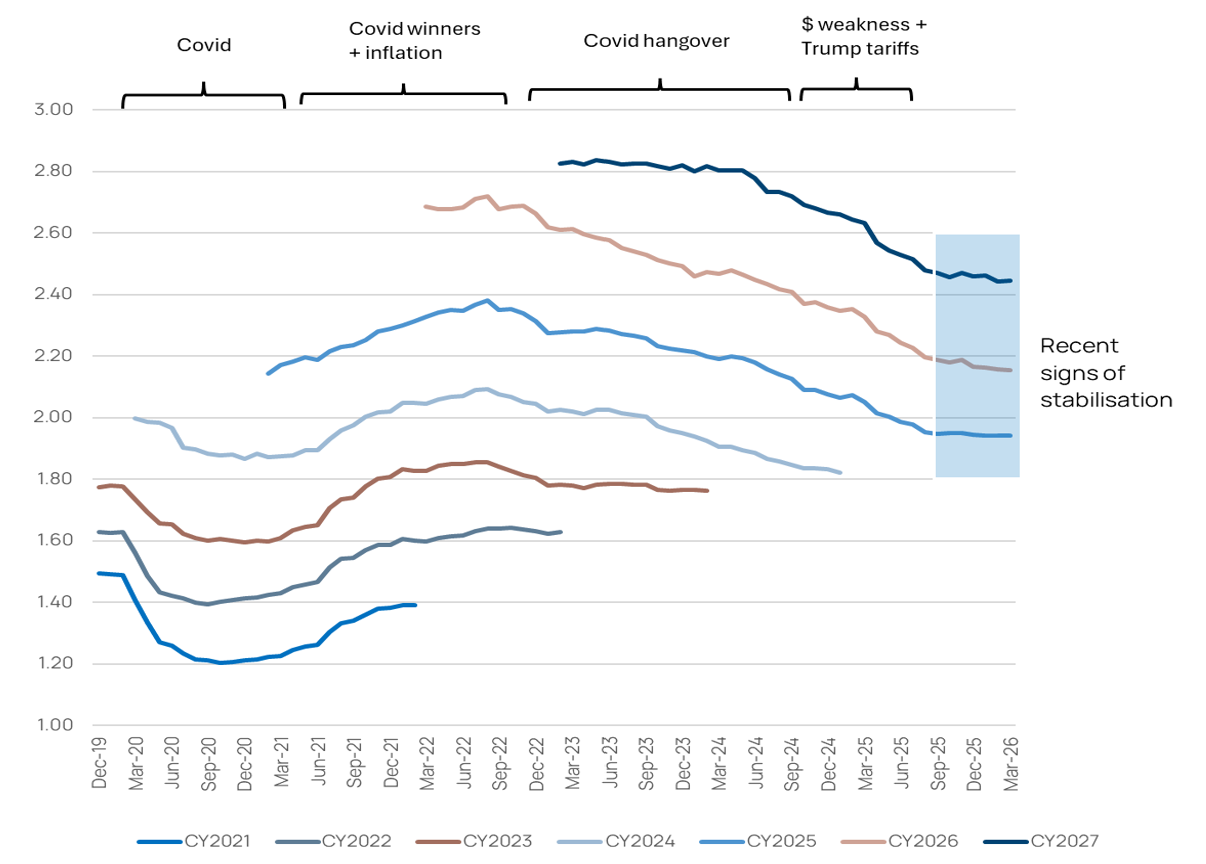

Wiggly Worms – continuing to show signs of stabilisation

In our December 2025 commentary we showed how earnings estimates for portfolio businesses had experienced a Covid boom and a post covid hangover, more recently suffering from the weak US Dollar and tariffs. At the time we noted recent signs of stabilisation. We updated the chart below to show that stabilisation has continued. The recent strengthening of the US Dollar is not yet reflected in these estimates and should provide further support.

Wiggly Worms: earnings estimates showing signs of stabilisation[2]

(Simulated back-test of the March 2026 portfolio)

Artificial Intelligence

AI remains a key focus. In the quarter, perceived AI victims (RELX, Experian, Amadeus, Dassault Systèmes, Adyen, combined 15%[3] of the portfolio) de-rated by between 20% and 40%, before partially rebounding. The market fears the phantom threat of AI and is selling indiscriminately. We are taking a more nuanced approach and have developed an AI Disruption Risk Index based on 10 software moats to appraise the AI risk (or opportunity) for each of our data and software businesses. Some moats are stronger than others in the AI era. Proprietary data, regulatory/compliance lock in and network effects are far stronger than workflow moats, public data and talent scarcity. As a result, we exited Accenture last year and added marginally to RELX and Experian during the sell-off earlier this year. The internet was a revolutionising technology in the late 1990s, and while it was disruptive to some, it was above all a powerful tool for those incumbents that adopted and adapted to it. We see AI in a similar way.

On the flip side, the portfolio has circa 15%3 exposure to businesses involved in the AI infrastructure build-out, from semiconductors, to datacenter power and networking leaders.

Portfolio Moves

During the quarter we took advantage of market volatility to trade more than usual. We exited Assa Abloy, Nemetschek and Novo Nordisk and built new positions in Ferrari and Richemont. These companies offer high-quality growth by combining scarce, heritage-driven brands with pricing power, loyal global customer bases, and controlled distribution, enabling high-margin, repeatable growth. We substantially increased our position in Halma, added to Sika and topped up RELX and Experian on weakness. We trimmed our semiconductor exposure (ASML, VAT and Seagate Technology) on price strength.

Outlook

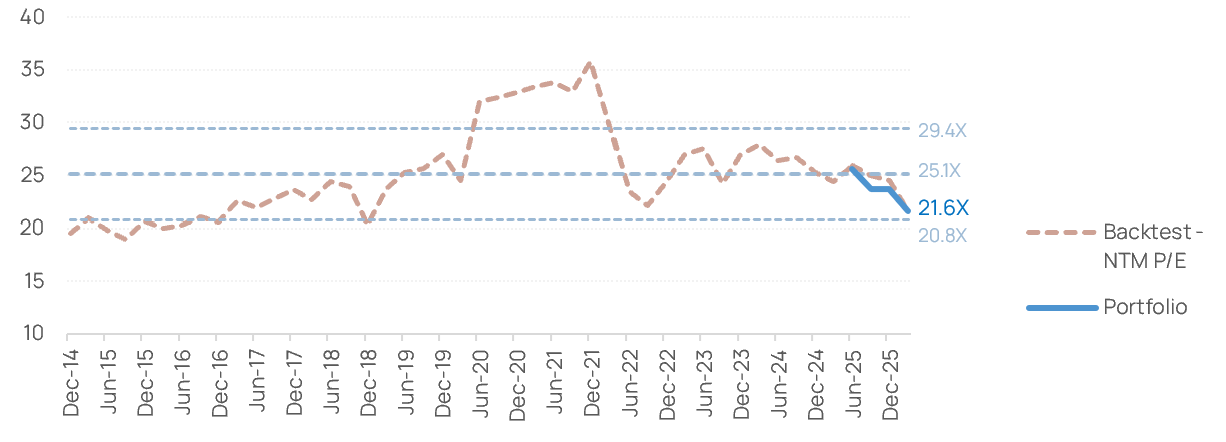

Valuations of quality businesses have continued to normalise from their 2021 peak. Comparing the valuation of today’s portfolio with its own simulated history, the portfolio in aggregate trades on a similar multiple today to what it would have done a decade ago, before quality-growth valuations expanded.

Simulated portfolio: valuation backtest – Current portfolio (NTM P/E) [4]

In the meantime, earnings estimates continue to show signs of stabilisation. We estimate low double-digit earnings per share growth for the coming 5 years, far above the MSCI Europe index. Our Total Shareholder Return model points to low-mid teens annual returns over the coming 5 years, with valuation no longer expected to be a headwind for the first time since the pre-covid era.

We thank you again for your interest in the Fund and warmly welcome you questions and comments.

Until next quarter,

Alistair, Arnaud & Sébastien

[1] S EUR ACC share class of the Aecus Europe Equity Fund

[2] Source: LSEG Workspace/Aecus Partners as of 26/03/2026.

Evolution of consensus next twelve months Earnings Per Share (NTM EPS) estimate for a given calendar year aggregated by asset weight at portfolio level of the Aecus Europe Equity Fund and based on LSEG Workspace market consensus. Portfolio weights as of 26 March 2026, rebalanced quarterly back in time. For any date of the simulation when a position was not yet listed, the portfolio was rebalanced excluding that stock. “CY”: Calendar Year.

[3] Portfolio weight as of 31 March 2026

[4] Source: LSEG Workspace/Aecus Partners as of 26/03/2026.

Note for the back-test: simulated Price to Earnings for the next twelve months (NTM P/E) using the portfolio of the Aecus Europe Equity Fund portfolio as of 26/03/2026. Portfolio weights as of 26 March 2026, rebalanced quarterly back in time. For any date of the simulation when a position was not yet listed, the portfolio was rebalanced excluding that stock. This does not reflect the actual portfolio P/E since launch, but a simulated calculation of a static portfolio measure for illustration purpose. The actual NTM P/E (ex-Cash) of the Aecus Europe Equity Fund since launch on 30/06/2025 is shown separately with the blue line.

Important Information

Issued by Aecus Partners SAS which is regulated by the Autorité des Marchés Financiers (AMF). RCS Paris n° 933 708 976 Agrément AMF n°GP20240027 (https://www.amf-france.org/fr, 17 place de la Bourse – 75002 Paris). The Fund is a sub-fund of the ICAV, an umbrella fund with segregated liability between sub-funds. The Fund is authorised by the Central Bank of Ireland as a UCITS pursuant to the European Communities (Undertakings for Collective Investment in Transferable Securities) Regulations. The ICAV has delegated UCITS management company functions to Aecus Partners SAS as its UCITS management company. The ICAV is authorised by the Central Bank of Ireland pursuant to the Regulations and the Central Bank (Supervision and Enforcement) Act 2013 (Section 48(1)) (Undertakings for Collective Investment in Transferable Securities) Regulations. The distributor of the Fund is Aecus Partners SAS. This financial promotion has been approved by Zeyro (FRN 1001386) on 15 April 2026. This Fund may be suitable for investors seeking long-term capital growth from European equities, who can commit to a five-year investment horizon and tolerate medium volatility and potential capital loss. It is not suitable for investors requiring capital protection, guaranteed returns, or access to capital within five years.

This document is a communication for information purposes only intended for professional clients. Please refer to the Fund’s prospectus and key information document before making any final investment decision. These documents are available free of charge, in paper or electronic format, from the Fund’s Investment Manager, as well as on the Manager’s website: https://www.aecuspartners.com. This material may not be copied, reproduced, communicated or redistributed, in whole or in part, without prior authorisation from Aecus Partners SAS. Any entity responsible for forwarding this material to other parties takes responsibility for ensuring compliance with applicable financial promotion rules. This material does not constitute a subscription offer and cannot be equated with a recommendation or investment advice. This material is not intended to provide, and should not be relied on for, accounting, legal or tax advice. This material has been provided to you for informational purposes only and may not be relied upon by you in evaluating the merits of investing in any securities or interests referred to herein or for any other purposes. Any specific securities identified and/or described in this document do not represent all of the securities purchased, sold, or recommended for the Fund and no assumptions should be made that the securities identified and discussed were or will be profitable. The information contained in this material may be partial information and may be modified without prior notice. It is not individually tailored for or directed to any particular client or prospective client. Prospective investors should consult their financial adviser before making an investment decision. The sources used to carry out this reporting are considered reliable, however no warranty of accuracy or reliability is given and no responsibility arising in any other way for errors and omissions (including responsibility to any person by reason of negligence) is accepted by Aecus Partners SAS, its officers, employees or agents. Aecus Partners SAS accepts no responsibility for any direct or indirect losses caused by the use of the information provided in this document.

All data is as at the document date unless indicated otherwise. Performance data herein relates to the Aecus Europe Equity Fund (the “Fund”). Net asset value performance (NAV) data has been calculated on a NAV-to-NAV basis and is net of management fees and operating expenses, with any income reinvested. A detailed description of the charges that apply is set out in the Prospectus. The ongoing charges figure may change over time. Company holdings and performance are likely to have changed since the report date. Company information, including performance calculations and other data, is provided by Aecus Partners SAS. Past performance may not be a reliable guide to future performance and investors may not get back the amount invested. If an investor’s own currency is different from the currency in which the Fund is denominated, the investment return may increase or decrease as a result of currency fluctuations. All investments involve risk. The value of the investment and the income from it will vary. The figures quoted relate to past periods and past performance is not a reliable indicator of future performance. The Fund uses the MSCI Europe Net Index (source: MSCI) as a comparator benchmark to compare performance. The Fund is actively managed and is not constrained by any benchmark. Glossary of terms: please refer to the website. Access to funds of an ICAV managed by Aecus Partners SAS may be subject to restrictions regarding certain persons or countries.

EEA – Access to the Fund may be subject to restrictions regarding certain persons or countries. The Fund’s Prospectus and KIDs can be obtained by visiting www.aecuspartners.com and are available in one of the official languages of each of the EU Member States into which the Fund has been notified for marketing under the Directive 2009/65/EC (the UCITS Directive). The Fund is currently notified for marketing into a number of EU Member States under the UCITS Directive.

UK – This Fund is a sub-fund of an Irish UCITS authorised by the Central Bank of Ireland and is not authorised by the UK Financial Conduct Authority (FCA). The Fund is recognised in the United Kingdom under the Overseas Funds Regime (OFR) in respect of certain share classes only. Only those share classes that have been recognised under the OFR may be marketed to investors in the UK. As an overseas fund recognised under the OFR, the Fund is not subject to UK sustainable investment labelling and disclosure requirements. The protections provided by the UK regulatory system, including access to the Financial Services Compensation Scheme (FSCS) and the Financial Ombudsman Service (FOS), do not apply. This document is for information purposes only and does not constitute an offer or solicitation to anyone in any jurisdiction in which such offer or solicitation is not authorised. Cancellation rights do not apply, and U.K. regulatory complaints and compensation arrangements may not apply. This material is issued and approved by Aecus Partners SAS which is authorised and regulated by the Autorité des Marchés Financiers (AMF).

Glossary of terms: please refer to the website

Contacts Aecus Partners: bonjour@aecuspartners.com – +33 (0)1 84 80 81 82 – 128 rue du Faubourg Saint-Honoré – 75008 Paris

Related insights

Insights

This section brings together Aecus Partners’ insights, perspectives and communications. It features a curated selection of content — podcasts, interviews, market updates and commentary — designed to share our views on portfolio companies and investment dynamics. These materials reflect our convictions at a given point in time, with the aim of providing a clear, structured and accessible perspective on complex topics.